All Categories

Featured

Table of Contents

For lots of people, the largest trouble with the infinite financial principle is that first hit to very early liquidity triggered by the expenses. This con of boundless banking can be lessened considerably with appropriate plan design, the first years will certainly always be the worst years with any Whole Life policy.

That said, there are certain boundless financial life insurance policy plans created mainly for high very early cash money value (HECV) of over 90% in the first year. However, the long-term efficiency will certainly usually considerably lag the best-performing Infinite Banking life insurance policy plans. Having access to that extra 4 numbers in the initial few years might come at the cost of 6-figures later on.

You in fact get some substantial long-term benefits that help you redeem these early expenses and afterwards some. We discover that this hindered very early liquidity issue with infinite financial is much more mental than anything else once extensively explored. Actually, if they absolutely needed every cent of the cash missing out on from their unlimited financial life insurance policy policy in the very first few years.

Tag: infinite financial concept In this episode, I speak about finances with Mary Jo Irmen who shows the Infinite Banking Concept. With the increase of TikTok as an information-sharing platform, economic advice and approaches have actually discovered an unique means of dispersing. One such strategy that has been making the rounds is the infinite financial concept, or IBC for short, gathering recommendations from celebs like rapper Waka Flocka Flame.

Within these plans, the cash money value expands based upon a price established by the insurer. As soon as a substantial money value builds up, policyholders can acquire a money value finance. These lendings vary from standard ones, with life insurance policy working as collateral, indicating one might lose their coverage if borrowing excessively without sufficient money worth to sustain the insurance policy prices.

And while the allure of these policies is obvious, there are innate restrictions and risks, demanding attentive money value surveillance. The method's authenticity isn't black and white. For high-net-worth individuals or business proprietors, specifically those making use of approaches like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and substance development could be appealing.

Becoming Your Own Bank

The attraction of limitless financial doesn't negate its challenges: Expense: The fundamental requirement, an irreversible life insurance policy policy, is costlier than its term counterparts. Qualification: Not everybody receives entire life insurance as a result of rigorous underwriting procedures that can leave out those with details wellness or way of living conditions. Complexity and threat: The elaborate nature of IBC, combined with its threats, might discourage numerous, specifically when less complex and less high-risk options are offered.

Alloting around 10% of your monthly earnings to the policy is just not practical for most people. Part of what you review below is simply a reiteration of what has already been said above.

Prior to you get on your own into a circumstance you're not prepared for, know the following first: Although the concept is commonly offered as such, you're not in fact taking a lending from on your own. If that were the situation, you would not need to repay it. Rather, you're borrowing from the insurer and need to repay it with rate of interest.

Some social media messages suggest making use of money worth from whole life insurance policy to pay down debt card debt. When you pay back the lending, a section of that passion goes to the insurance policy firm.

For the first a number of years, you'll be paying off the payment. This makes it exceptionally difficult for your plan to gather value during this time. Unless you can manage to pay a few to a number of hundred dollars for the following decade or even more, IBC won't function for you.

Infinite Banking Insurance Companies

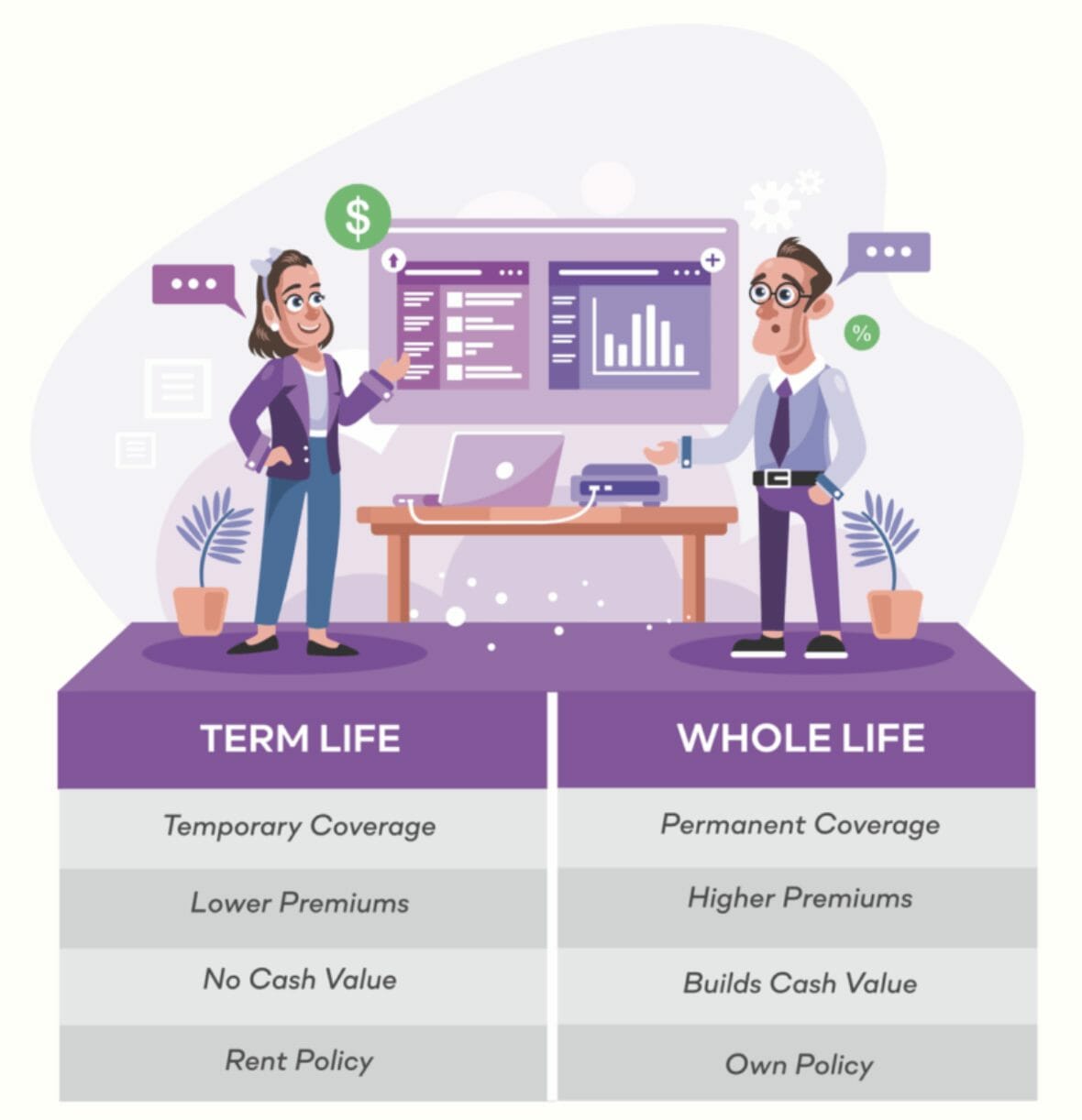

Not every person must depend solely on themselves for monetary safety and security. If you require life insurance policy, right here are some useful pointers to think about: Consider term life insurance. These plans offer coverage during years with significant monetary responsibilities, like home mortgages, trainee car loans, or when taking care of young youngsters. Ensure to look around for the best price.

Copyright (c) 2023, Intercom, Inc. () with Booked Font Style Call "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Font Style Call "Montserrat".

Infinite Banking Insurance Agents

As a CPA concentrating on property investing, I've cleaned shoulders with the "Infinite Financial Principle" (IBC) a lot more times than I can count. I've also interviewed professionals on the subject. The primary draw, besides the evident life insurance coverage benefits, was constantly the concept of building up money worth within a long-term life insurance policy plan and loaning against it.

Certain, that makes good sense. Yet truthfully, I always thought that cash would certainly be much better spent straight on financial investments instead of channeling it via a life insurance policy policy Until I found how IBC can be combined with an Irrevocable Life Insurance Policy Depend On (ILIT) to produce generational riches. Let's start with the basics.

Paradigm Life Infinite Banking

When you borrow against your policy's cash money value, there's no set repayment routine, offering you the liberty to take care of the finance on your terms. The money value continues to grow based on the policy's assurances and returns. This configuration permits you to gain access to liquidity without interrupting the lasting development of your policy, gave that the finance and rate of interest are taken care of wisely.

The procedure continues with future generations. As grandchildren are born and expand up, the ILIT can buy life insurance policies on their lives. The trust fund then accumulates numerous plans, each with expanding cash money worths and death advantages. With these plans in place, the ILIT efficiently becomes a "Family Financial institution." Member of the family can take fundings from the ILIT, utilizing the cash value of the plans to money investments, start companies, or cover significant expenditures.

An essential element of handling this Family members Financial institution is making use of the HEMS criterion, which means "Health and wellness, Education And Learning, Maintenance, or Assistance." This standard is often consisted of in count on agreements to direct the trustee on how they can disperse funds to recipients. By adhering to the HEMS criterion, the count on makes sure that circulations are produced necessary needs and lasting support, guarding the trust fund's properties while still offering household members.

Increased Adaptability: Unlike stiff small business loan, you control the repayment terms when borrowing from your very own policy. This allows you to framework payments in a method that straightens with your company cash circulation. how can i be my own bank. Enhanced Cash Circulation: By financing service expenses with plan car loans, you can possibly liberate cash that would otherwise be locked up in conventional finance settlements or tools leases

He has the same equipment, however has actually also developed added money value in his plan and obtained tax obligation benefits. Plus, he currently has $50,000 offered in his policy to use for future possibilities or expenditures., it's crucial to see it as even more than just life insurance.

Infinite Bank Concept

It has to do with developing an adaptable financing system that gives you control and supplies numerous benefits. When utilized tactically, it can enhance various other financial investments and business techniques. If you're fascinated by the capacity of the Infinite Financial Principle for your company, here are some steps to consider: Inform Yourself: Dive deeper right into the principle with trusted books, workshops, or consultations with educated experts.

{kind=link}

Latest Posts

Self Banking Whole Life Insurance

Infinite Wealth And Income Strategy

Nelson Nash Bank On Yourself